I recently attended the massive PRI conference in Paris with 1,800 participants. Below are my takeaways from there and other things I have learned.

The leading theme of the conference was “urgency in transition” — how the shift to a low-carbon economy must happen, and soon. The second overarching theme was active ownership and owner engagement. The third theme in focus was the significance of ESG in real assets, particularly in real estate — the potential for impact in mitigating climate change is substantial.

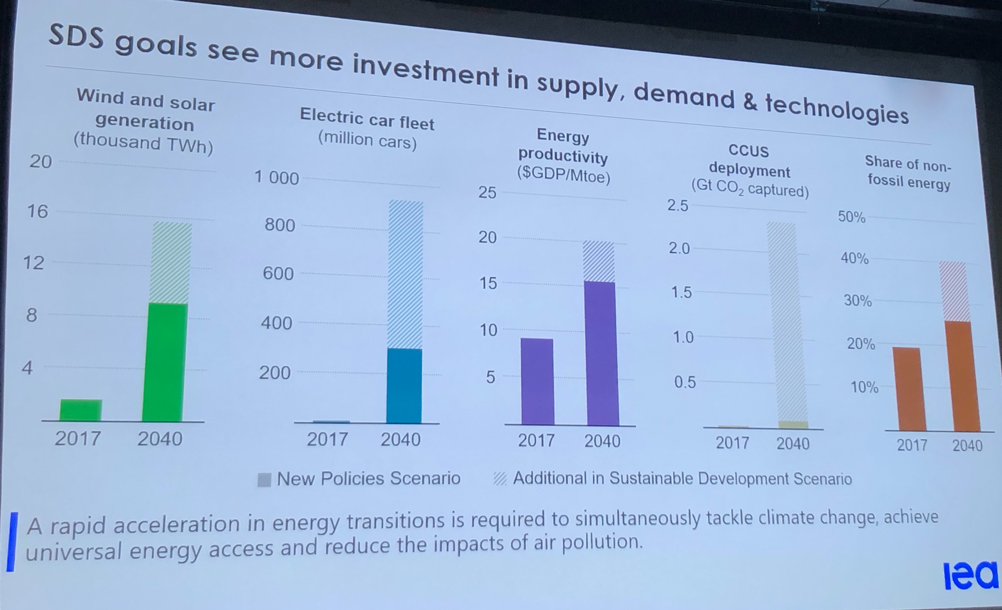

URGENCY IN THE TRANSITION TO LOW CARBON

Shell’s CEO Ben van Beurden described to the audience how Shell has publicly committed to halving its carbon footprint by 2050. CO2 emission targets are already taking effect this year for oil and gas operations as well as product sales, with the goal of falling 2%-3% below the 2016 level by 2021. The targets are being linked immediately to executive compensation and will later be extended to 16,000 employees. The emission target covers the combined total of Scope 1 (own operations), Scope 2 (purchased energy), and Scope 3 (indirect emissions).

Van Beurden made the excellent point that the company cannot reach its targets alone if its customers do not reach theirs, and he described how Shell is planning together with key players such as airports and aircraft manufacturers on how to achieve the targets. Van Beurden called for this collaborative approach across different industries, as it is the way to make practical progress: regulators can then focus on setting broader guidelines. In Finland, Minister Kulmuni recently brought this industry roadmap thinking into the public discourse.

Enel’s CFO Alberto de Paoli: “Sustainability is our business, we do not have any other business”. He described how the UN Sustainable Development Goals have been adopted as the foundation of the company’s entire strategy, thereby turning financial performance from losses into strong growth. Enel has prioritised 4 SDGs and recently issued a 4-billion-euro SDG bond.

New low-carbon benchmarks are expected to come into force as early as April 2020, which will direct capital at record speed towards environmentally friendly economic activities (underpinned by the EU taxonomy’s new definitions).

How to accelerate capital allocation to sustainable targets?

A distinguished panel discussed the decisive importance of Strategic Asset Allocation (SAA) in directing funds towards sustainable targets. Behind allocation limits lie the return expectations for different asset classes, which are often also short-term expectations. Are these wrong? Have the sector expectations underlying equity markets been unpacked (for example, the deteriorating return expectations for the oil and gas industry and the automotive industry)? And are the expectations too linear when change is happening rapidly? The panel was unanimously ready to transform SAA into SRA, that is, “Sustainability Risk Allocation”.

Sustainability cannot be just an isolated component of investment plans. Should the physical and transition risks related to climate change, as described in the TCFD* framework, be part of an institution’s risk policy description? This would mean that their significance in the portfolio would need to be assessed. In that case, reporting on climate change-related risks and opportunities (the TCFD report) would also arise naturally. Wellington: “The market focuses more on transition risk rather than actual physical risk, which is our focus — both are important, and one must be able to distinguish between them.”

(*TCFD, the Task Force on Climate-related Financial Disclosures, divides risks into physical risks — for example, sudden damage caused by extreme weather events such as droughts or heavy rainfall — and transition risks, which concern the fact that the shift to a low-carbon economy entails changes in regulation, technology, and consumer behaviour, among other things. These in turn affect companies’ cash flows and consequently their return outlooks. On the other hand, climate change also brings opportunities for investors.)

THE RISE OF ACTIVE OWNER ENGAGEMENT

Ownership has moved to centre stage — not just at the PRI conference. When I met an old friend who long served as CEO of the asset management firm DWS (Deutsche Bank’s most valuable asset), we discussed DB’s situation. The bank’s largest owners include BlackRock, Vanguard, and CalSTRS. The question is which of these owners has the capacity and time to consider the bank’s strategy and find its most competent leadership, as these are among the key responsibilities of owners. In the march of passive funds, active ownership and owner engagement — which require experience and wisdom — are often left behind.

At the PRI owners’ workshop, it was reported that a large proportion of asset managers did not support the inclusion of purpose for the economy in the new UK Stewardship Code, whereas owners did support it. This illustrates the ambiguity surrounding active owner engagement: is it the task of the asset manager or the owner? Among the governance codes of different countries, the UK code is the most widely adopted. The definition of the recently approved stewardship code is: “The responsible allocation, management and oversight of capital to create long-term value for clients and beneficiaries leading to sustainable benefits for the economy, the environment and society”.

The code aims to increase owner engagement in governance and to take into account beneficiaries’ (typically long-term) investment horizons in making investment decisions. The code clearly references ESG factors. The code requires its signatories to report on their own purpose, values, and culture, as well as how they use their resources, rights, and influence in governance. Unlike its predecessor, the code extends beyond listed equities to private equity investments. The code applies to asset owners, asset managers, and service providers. Finland lacks such an investment stewardship code.

- Wellington: Investment stewardship and active ownership relate to every stock; the market focuses more on transition risk rather than actual physical risk, which is Wellington’s focus; all indices focus on the past.

- Investors and asset managers have “one hand on the wheel” — 99 percent of the budget spent on asset management is allocated to allocation and 1 percent to stewardship. Passive houses are in a sense universal investors that should take responsibility.

- The old concept of the “universal investor” has been revived: the world’s largest pension fund, Japan’s Government GPIF, as well as Norway’s oil fund and other truly large investors have begun cooperating (“soft power”) particularly to mitigate climate change. They can operate across borders, and part of their return comes from combating systemic risk through their actions. GPIF’s CIO Hiro Mizuno (pictured below) pointed out that general attention focuses on generating Alpha, when instead one should safeguard Beta: “I am prepared to change the system, the returns come from the system. GPIF wants to save the Beta.”

As an example, Mizuno described how he has required Toyota and other major corporations to report in accordance with the TCFD. They in turn require the same from their subcontractors. This is the reason why Japan has surprisingly risen to the top globally as a TCFD signatory country. Mizuno also described how GPIF has conducted its first-ever climate risk assessment. He admitted he does not know whether the methodology is correct and urged listeners to undertake such an assessment: “Do not strive for perfection — when you are among the first, your approach becomes best practice.” GPIF focuses on transition risk analysis.

When companies first begin collecting data and then reporting systematically on, for example, carbon emissions, only after that is it possible for them to set targets for reducing emissions. And investors in turn receive information to support decision-making when they want to reduce carbon intensity in their portfolios.

One indicator in evaluating a company is whether it has begun reporting in accordance with Science Based Targets, that is, seriously pursuing alignment with the goals of the Paris Climate Agreement.

- In a conversation with the CIO of Allianz, I mentioned that I often hear that an institution’s investment is “just” a financial investment, and therefore engaging on ESG matters is not relevant. He responded immediately that especially when ESG matters are not in order, regardless of the size of the investment, the owner must act to get them in order. In other words, there is no minimum threshold below which an investment can be called merely a financial investment from an ESG perspective. This answer was surprising.

- Sweden’s AP1, as a large pension company, has taken the bull by the horns and established a global project called “Investing in Just Transition”, for which they have also obtained external funding. The main objective is to influence companies to reduce their emissions and to act as an active owner so that capital is allocated correctly. They have selected companies from which they demand clear reduction targets and engage in rigorous dialogue with them on the subject. Clear results are visible.

- At the conference, an award was given to a pension company that had asked its beneficiaries which SDGs are important to them, after which they instructed their asset managers accordingly in investment activities. This was considered impact at its best.

A strong theme that emerged at the PRI conference was that instead of general sustainability discussion, efforts should be made to measure ESG impact, which begins with examining and observing exposure to various sustainability questions and then determining how the identified issues are managed, especially when the associated risk is high. Outcomes and conclusions were called for instead of general talk.

It was clearly visible that the focus had shifted from footprint — that is, how things are done — to handprint — that is, what is done.

TCFD REPORTING IN JAPAN

In week 41, I attended an event in Tokyo organised by the TCFD, Japan’s Ministry of Economy, Trade and Industry (METI), and the World Business Council for Sustainable Development (WBCSD), where representatives of Japanese companies were guided on TCFD reporting.

The seminar, pictured above, was full of company representatives who carefully reviewed the TCFD reporting guidelines and examples prepared by SASB. The information was taken seriously, and questions poured in. Pictured is SASB’s Director of Research David Parham, participating in describing sector-specific reporting topics and metrics found in SASB’s global ESG standard for companies, including financial sector actors.

|

|---|

| SASB’s Director of Research David Parham at the Finnish Embassy in Tokyo |

Tracefi also organised an investor event with SASB during that week at the Finnish Embassy in Tokyo, where Parham served as one of the presenters. Topics included climate risk assessment, TCFD reporting, ESG reporting, and its communication. The discussion was open and constructive. Parham shared that of SASB’s 77 industries, climate change affects 69 in the form of physical, transition, or regulatory risk. He described how the SASB standard can be used to analyse the overall impact of climate change. Parham considered the UN Sustainable Development Goals to be very important for all market participants: “When the SDG target creators have already laid out the path for investors showing how companies can contribute to the goals, it would be wise to use this path.”

I shared that at Tracefi we have used the TCFD framework in advising on the development of sustainability policies and related targets, and asked whether this is the right approach. Parham responded: “Of course, what else could it be?”

|

|---|

| Senior General Manager Mafumi Tamaoki and Senior Portfolio Advisor Mayuko Hoshikawa from Nissay Asset Management |

Japanese guests, representing firms including Nissay and Sumitomo Mitsui Trust Asset Management, Mitsubishi Trust, and Daiwa Institute of Research, viewed Europe as a pioneer in sustainable finance. Japan is closely following the EU’s taxonomy development, and progress is rapid. I presented Tracefi’s methodology for assessing portfolio ESG risks and opportunities as well as SDG impacts. We also discussed sustainability from the perspectives of the board and the individual.

The clear message from the events was that alongside investment policy, sustainability policy needs to be developed for evaluating investments, with a particular focus on concrete target-setting by the board that it can monitor. That is where change begins. The impact of emissions on investments, risks from physical and regulatory changes, and transition risks need to be assessed for all investments. Considering the impacts of climate change and taking action on climate change will soon no longer be optional, as there are few industries for which climate risks could be disregarded.

Please get in touch if these topics interest you. Autumn greetings,

Susanna